A few years ago, I was wrapping up a massive web development contract for a high-profile e-commerce client. I felt like a rockstar. The site was beautiful, the custom code was sleek, and we were days away from launching their seasonal product line.

During the final sign-off meeting at their beautiful downtown office, I reached for my coffee mug and clumsily knocked it straight into the client’s brand-new, top-of-the-line MacBook Pro. There was a horrifying sizzle, a flash of static on the screen, and then dead silence.

I was mortified. But I remember thinking, “Thank God I bought that general liability insurance policy last month.” I called my provider, filed a property damage claim, and they took care of replacing the ruined hardware. Easy, right?

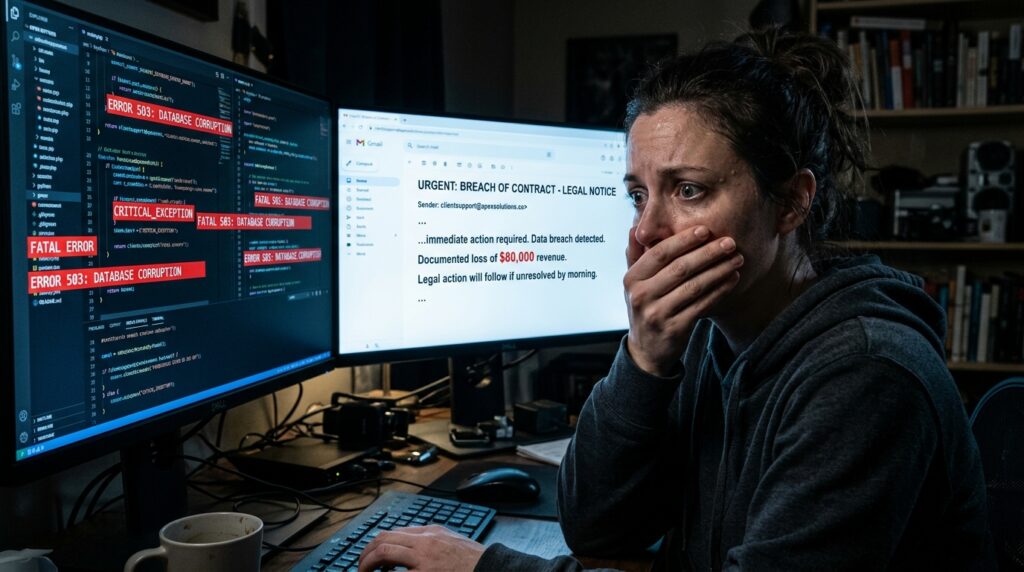

But here is the twist: what if I hadn’t spilled coffee? What if, instead, a logical error in my custom checkout code had quietly glitched during launch week, crashing their payment gateway and costing them $80,000 in lost holiday sales?

If that client had sued me to recover their lost revenue, my General Liability policy wouldn’t have paid a single dime. I would have been completely exposed.

That was the moment I truly understood the massive, hidden canyon separating General Liability and Professional Liability insurance. Too many small business owners, freelancers, and consultants treat these two policies like they’re interchangeable variations of “lawsuit protection.” They aren’t. Choosing the wrong one can leave your entire life savings completely unprotected.

Let’s skip the confusing legal jargon and look at the real-world differences between these two coverages, how they work in practice, and how to figure out exactly what your business needs.

The Core Difference: Physical vs. Financial Disasters

The absolute simplest way to tell these two policies apart is to look at the nature of the damage that occurred.

- General Liability protects your business against physical disasters. Think of it as coverage for accidents involving tangible things—bodies getting hurt or physical property getting broken.

- Professional Liability (often called Errors & Omissions, or E&O) protects your business against financial or strategic disasters. It covers mistakes made in your advice, your designs, your code, or your specialized services that cause a client to lose money.

┌─────────────────────────────────────────────────────────┐

│ THE CORE DIFFERENCE │

└─────────────────────────────────────────────────────────┘

│ │

▼ ▼

GENERAL LIABILITY PROFESSIONAL LIABILITY

"Physical Disasters" "Financial Disasters"

• Slips and falls • Missed deadlines

• Broken equipment • Professional mistakes

• Bodily injury claims • Bad strategic advice

Deep Dive: General Liability Insurance

General Liability is almost always the very first policy a small business buys. In fact, if you rent a commercial office space, sign a contract with a corporate client, or apply for a local business license, you are almost always legally or contractually mandated to show proof of this coverage.

It covers three main buckets of risk:

1. Third-Party Bodily Injury

This is your classic “slip-and-fall” scenario. If a delivery driver trips over an loose extension cord in your studio, cracks their knee, and requires emergency room treatment, your general liability policy steps in to cover their medical bills and your legal defense if they decide to sue. (Note: This only covers customers or visitors, not your own employees—that’s what Workers’ Comp is for).

2. Third-Party Property Damage

Like my infamous coffee spill incident, this kicks in if you or an employee accidentally damages someone else’s physical stuff while conducting business. If you are a house cleaner and drop an expensive crystal vase, or a contractor putting a foot through a homeowner’s drywall, this is your safety net.

3. Advertising Injury

This covers non-physical blunders like libel, slander, or accidental copyright infringement in your marketing materials. If your business runs an Instagram ad that inadvertently uses a competitor’s copyrighted image or slogan, and they slap you with a lawsuit, General Liability helps pay the lawyers.

Average Cost Check: For most low-risk small businesses, freelancers, or online entrepreneurs, a standard $1 million General Liability policy is incredibly affordable, usually running between $40 and $100 per month.

Deep Dive: Professional Liability (E&O) Insurance

Professional Liability is all about the quality of your intellect, expertise, and execution. If your business gets paid to think, advise, design, build digital assets, or provide specialized care, you face a completely different set of risks that have nothing to do with physical accidents.

If you make an honest mistake that hits a client directly in their bank account, they don’t care about a coffee spill—they care about their bottom line. Professional Liability steps in to cover:

1. Professional Negligence or Mistakes

You are human, and eventually, a mistake will slip past your quality control checklist. If an accountant transposes two numbers on a major corporate tax filing, causing the client to face massive IRS fines, Professional Liability covers the fallout.

2. Misrepresentation or Breach of Contract

If you sign a contract promising to deliver a custom software platform by October 1st so a client can launch their holiday marketing push, but unexpected bugs push your launch date back to January, that client can sue you for breach of contract to recover the massive revenue they missed out on.

3. Oversight and Omissions

Sometimes it’s not what you did, but what you forgot to do. If a home inspector overlooks a massive foundation crack hidden behind some drywall, and the new homeowner faces a $30,000 repair bill a month after moving in, they will sue the inspector for an omission of critical facts.

Average Cost Check: Professional liability rates vary wildly depending on how high-stakes your industry is. A business consultant might pay $35 to $60 a month, while a structural engineer or a medical professional will face significantly higher premiums due to the severe financial or physical impact of an error.

Real-World Use Cases: Which One Kicks In?

To see how these two policies operate side-by-side, let’s look at three common industries to see exactly how a crisis maps to a specific policy.

Scenario A: The Graphic & Web Designer

- The Incident: You invite a premium client to your home studio to look at mood boards. They trip over the edge of an area rug, fall, and break their wrist.

- Which policy responds? General Liability (Third-party bodily injury).

- The Incident: You mistakenly use an unlicensed font on a client’s global packaging rollout. The font owner discovers it and forces your client to recall $100,000 worth of printed inventory. The client sues you to recover the printing costs.

- Which policy responds? Professional Liability (Copyright oversight/Professional mistake).

Scenario B: The IT Consultant / Developer

- The Incident: While working on-site at a client’s server room, you accidentally knock over an expensive network rack, shattering thousands of dollars of hardware.

- Which policy responds? General Liability (Property damage).

- The Incident: You write a bad script during a routine database migration that completely deletes a client’s live user accounts, causing their subscription platform to go dark for two full days. They sue you for the lost subscriber revenue.

- Which policy responds? Professional Liability (Errors & Omissions).

Scenario C: The Fitness Trainer

- The Incident: A client drops a heavy dumbbell on their foot because the gym floor was slick from an oil spill you didn’t wipe up.

- Which policy responds? General Liability (Premises liability).

- The Incident: You design a highly aggressive custom workout and nutrition plan for a client with a documented medical condition. The plan triggers a severe health crisis, and they sue you for providing improper professional guidance.

- Which policy responds? Professional Liability (Professional negligence).

Common Mistakes to Avoid When Buying Coverage

- Assuming a BOP Covers Everything: A Business Owner’s Policy (BOP) is a fantastic, highly discounted bundle that combines General Liability with Commercial Property insurance. However, a standard BOP does not automatically include Professional Liability. You almost always have to add it as a specific policy rider or buy a separate standalone policy.

- Waiting Until You Get Sued to Shop Around: Insurance companies use your clean history to give you the sharpest rates. If a client is already threatening a lawsuit via email, you cannot quickly buy a policy today and expect it to cover yesterday’s mistake. Insurers look closely at the “Prior Acts” or retroactive date on your policy.

- Hiding Your Real Services to Get a Cheaper Premium: When filling out quotes on platforms like Next Insurance, Progressive Commercial, or Hiscox, don’t list your business as a “writer” if you actually do high-end software development or financial consulting just because the premium looks cheaper. If a claim arises and the insurer realizes you misrepresented your core operations, they will immediately void your claim and cancel your policy.

Step-by-Step: How to Choose Your Setup

If you want to make sure your small business is completely bulletproof without blowing your budget, follow this quick checklist:

- Map Your Delivery Model: Do you interact with people or their physical objects in real life? If yes, start with General Liability immediately.

- Map Your Intellectual Risk: Do people pay you for your knowledge, your technical execution, or your creative deliverables? If yes, secure a Professional Liability quote alongside your baseline coverage.

- Check for Bundle Options: Ask an independent commercial broker if your specific industry classification allows you to attach a Professional Liability endorsement straight onto a basic Business Owner’s Policy (BOP). This is almost always significantly cheaper than buying two entirely separate, standalone products.

Final Thoughts

At the end of the day, commercial insurance isn’t just a boring regulatory hurdle or a waste of monthly cash. It’s an investment in your peace of mind.

Knowing the distinction between a physical mishap (General Liability) and an intellectual error (Professional Liability) lets you build an exact, customized shield around your business. Take an hour out of your schedule this week to audit your active contracts, look over your current declarations page, and fill in any gaps before an expensive mistake forces your hand.