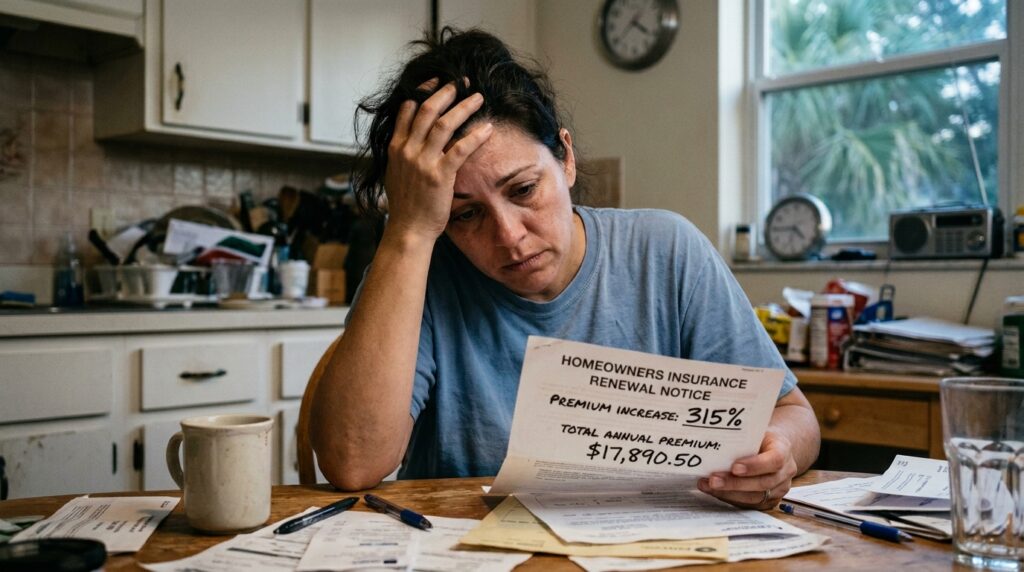

A few weeks ago, I opened a completely unremarkable, white window envelope from my insurance company. Inside was my renewal notice. I expected a slight bump—maybe a few hundred bucks to account for standard inflation.

Instead, my eyes locked onto a number that genuinely made my stomach drop. My annual premium had shot up by nearly 40%. No claims filed. No dynamic additions to my house. No changing risk on my end. Just a massive, looming expense that felt like a secondary mortgage.

If you own a home in Florida, you already know this story. You are likely living it.

Right now, Floridians are paying an average of nearly $11,000 a year for home insurance—which is roughly 180% higher than the national average. It’s a full-blown financial crisis quiet-quitting its way into our family budgets.

As a tech and real estate blogger who obsesses over data and practical optimization, I couldn’t just sit back and take the hit. I spent the last month digging into the “why” behind these astronomical rates and, more importantly, testing real-world strategies to bring my own bill down.

Here is exactly what is happening behind the scenes in the Florida insurance market, the real reasons your premium is so high, and the exact steps you can take right now to claw some of that money back.

The “Perfect Storm” Driving Florida Insurance Rates

It’s easy to blame the weather, and yes, our beautiful, vulnerable peninsula sits directly in the crosshairs of intense Atlantic and Gulf hurricane tracks. The catastrophic damage from back-to-back major storms left a massive financial dent in the insurance sector. But weather is only a fraction of the equation.

If it were just about hurricanes, states like Texas and Louisiana would have identical pricing curves. Florida’s crisis is unique because it is driven by three man-made systemic issues.

1. The Hidden Cost of Reinsurance

Insurance companies don’t hold all the risk themselves. They buy their own insurance, known as reinsurance, from massive global entities to ensure they don’t go bankrupt after a Category 5 storm hits a major metro area.

Because global climate disasters have spiked and general inflation has climbed, the cost of reinsurance has skyrocketed over the past few years. When a local Florida insurer has to pay double for its own reinsurance coverage, that massive bill gets directly divided up and tacked onto your premium notice.

2. A Legacy of Systemic Litigation Abuse

For over a decade, Florida was a legal anomaly. The state historically accounted for roughly 8% of all homeowners’ insurance claims nationwide, but a staggering 79% of all homeowners’ insurance lawsuits took place here.

This was heavily driven by scams surrounding “Assignment of Benefits” (AOB). Unscrupulous contractors would knock on doors after a minor storm, promise a “free roof,” ask the homeowner to sign over their insurance rights, and then sue the insurance company for an inflated payout.

While landmark legislative reforms passed between 2022 and 2024 have finally banned AOB abuse and ended one-way attorney fees, the market is still recovering from the financial bleeding of the previous decade.

3. Skyrocketing Rebuilding Costs

Think about what it costs to hire a contractor or buy building materials today versus four years ago. According to recent construction data, building material costs and skilled labor wages have surged dramatically.

Insurers use automated replacement cost software to estimate what it would take to rebuild your home from scratch if it burned down tomorrow. Because materials and labor are so expensive, your home’s calculated “replacement value” went up, forcing your premium up with it.

The Mistake That Cost Me Hundreds

When I first looked into lowering my premium, I made a classic rookie mistake: I immediately went online and checked the box to raise my standard deductible to the absolute maximum allowed, assuming it was the fastest way to save.

Don’t just blindly slide the deductible bars around without doing the math. In Florida, you typically have two distinct deductibles:

- All Other Perils (AOP): Covers standard things like a kitchen fire, a burst pipe, or theft.

- Hurricane Deductible: This is calculated as a percentage of your home’s total insured value (usually 2%, 5%, or 10%), not a flat dollar amount.

If your home is insured for $400,000 and you foolishly set a 10% hurricane deductible to save a few hundred bucks on your annual premium, you are agreeing to pay the first $40,000 out of pocket before your insurance pays a single dime for storm damage.

I quickly realized that shifting too much risk onto my own shoulders wasn’t solving the problem; it was just setting a financial landmine for the next hurricane season. I rolled that change back and looked for smarter, structural ways to cut costs.

Action Plan: How to Drop Your Florida Insurance Bill

If you want to see real relief, you have to be proactive. Sitting around waiting for policy prices to drop naturally isn’t a winning strategy. Here is the exact checklist I used to aggressively optimize my policy.

1. Order a Fresh Wind Mitigation Inspection

If you take only one piece of advice from this guide, make it this one. In Florida, insurers are legally mandated to give you premium credits if your home has documented features that help it resist high wind speeds and flying debris.

A standard wind mitigation inspection costs between $95 and $150 and takes less than an hour. A licensed inspector will check six critical structural areas:

| Structural Feature | What the Inspector Looks For | Why It Saves You Money |

| Roof Shape | Hip roofs (sloped on all four sides like a pyramid) vs. flat Gable roofs. | Hip roofs naturally divert wind upwards and take significantly less damage, triggering massive premium discounts. |

| Roof Deck Attachment | The thickness of the plywood and the length/spacing of the nails holding it down. | Tighter nail spacing means the roof deck is less likely to peel off during high winds. |

| Roof-to-Wall Connection | The presence of metal hurricane straps or clips connecting the roof to the walls. | Keeps the entire roof structure securely anchored to the house frame under extreme uplift pressure. |

| Secondary Water Resistance | A self-adhesive waterproof barrier applied directly beneath your shingles or tiles. | Prevents catastrophic water intrusion even if your top shingles get ripped off by a storm. |

| Opening Protection | Impact-rated windows, exterior doors, and garage doors, or approved storm shutters. | Prevents a window from breaking, which can pressurize the inside of the house and literally blow the roof off. |

Many homeowners have older, outdated wind mitigation reports on file, or have made minor home upgrades without submitting a new report. When I updated mine, my inspector documented that my roof-to-wall connections used proper clips rather than old-school toenails. That single update saved me hundreds on the windstorm portion of my bill.

2. Tap into the “My Safe Florida Home” Program

If your wind mitigation report reveals that your home lacks critical storm protection, do not pay for these massive structural upgrades entirely out of pocket.

The Florida Legislature replenished the My Safe Florida Home program with hundreds of millions of dollars in fresh funding. This state-backed program offers homeowners:

- Free wind mitigation inspections to pinpoint vulnerabilities.

- Matching grants (up to $10,000) where the state contributes $2 for every $1 you spend on qualifying home hardening improvements, like upgrading to an impact-rated garage door or replacing an aging roof.

Hardening your home through this program provides a double financial win: it directly lowers your risk of catastrophic property damage, and it forces your insurance company to slash your premium via wind mitigation credits.

3. Shop the Easing Market via an Independent Agent

For a few years, shopping around for insurance in Florida was completely futile. Private carriers were going insolvent or fleeing the state, leaving Citizens Property Insurance (the state-backed “insurer of last resort”) as the only option for millions.

However, the tide is starting to turn. Thanks to recent legal reforms, reinsurance costs are stabilizing, and new private domestic carriers are entering the Florida market.

Do not use captive agents who only write policies for a single company. Work exclusively with an independent insurance agent who has access to multiple carriers. Have them run your updated wind mitigation data through their comparative rater software. You might be surprised to find a hungry new private insurer willing to underbid your current policy just to build their Florida book of business.

4. Strip Out Unnecessary Add-ons

Take a close look at the line-item breakdowns on your policy’s declaration page. Insurers love to bundle in auxiliary coverages that you might not actually need.

For example, do you have a massive coverage limit for “Other Structures” (Coverage B)? If you don’t have a detached guest house, a massive shed, or an expensive gazebo, you are paying to protect assets that don’t exist. Ask your agent to drop that coverage down to the legal or structural minimum.

What Not to Do: The Danger of Going Uninsured

As premiums climb, a dangerous trend is emerging across the state: homeowners who have paid off their mortgages are choosing to drop their insurance completely and “go bare.”

Unless you have millions of liquid dollars sitting in a bank account to completely rebuild your lifestyle from scratch after a total loss event, this is an incredibly risky gamble. A standard homeowner’s policy doesn’t just protect four walls and a roof; it provides critical personal liability protection if someone gets injured on your property, and it covers your temporary living expenses if a disaster renders your home unlivable.

Instead of walking away from coverage entirely, focus your energy on structural risk reduction, utilizing state grant money, and shopping the newly stabilizing private market. By being proactive and treating your home insurance like a data-driven optimization problem, you can safely protect your greatest financial asset without emptying your savings account.