A few years ago, I fell into the ultimate auto-renewal trap. I was busy with a major project launch, and when my health insurance company sent me that standard autumn email stating, “No action needed! Your plan will automatically renew for next year,” I breathed a sigh of relief. I ignored it and let the machine roll over.

That single bit of laziness cost me nearly $1,400 out of pocket over the next twelve months.

When January arrived, I discovered that my plan’s co-insurance split for specialist visits had jumped from 20% to 40%, two of my prescription medications had been booted off the approved “formulary” list, and my preferred local urgent care clinic was no longer in-network. The insurance company hadn’t lied; they did auto-renew me, but they auto-renewed me into a structurally modified, more expensive version of the policy.

The lesson hit hard: In the health insurance world, inertia is an active financial penalty.

With sweeping changes rolling out across the national exchanges, navigating the upcoming Open Enrollment cycle requires your undivided attention. Whether you rely on an employer-sponsored plan, use an individual Affordable Care Act (ACA) Marketplace option, or manage Medicare, here is the field-tested playbook on the critical deadlines, optimization tips, and best-performing plans you need to secure your safety net.

The Master Clock: Crucial Deadlines You Cannot Miss

Missing an enrollment deadline isn’t like missing a credit card due date—you can’t just pay a $35 late fee and move on. If you miss these windows, you are legally locked out of purchasing compliant health coverage for the entirety of the calendar year, unless you experience a major qualifying life event (like losing a job, getting married, or having a child).

The industry timelines are highly specific across the different insurance channels:

1. The ACA Marketplace (Obamacare / HealthCare.gov)

For individual plans purchased independently on the federal or state exchanges, the open enrollment window remains structured across a tight winter window. However, pay close attention to the effective date split:

- November 1: The official starting line. This is the very first day you can log onto the exchange to compare prices, update your household income details, and actively select a new plan.

- December 15: The most critical deadline on the calendar. If you want your new healthcare coverage to actively kick in on January 1, you must bind and fund your policy by midnight on this exact date.

- January 15: The absolute closing gate. This is the final day to select an individual plan for the year. If you enroll between December 16 and January 15, your health coverage will not become active until February 1, leaving you completely exposed for the entire month of January.

2. State-Specific Deviations

If your state runs its own independent exchange infrastructure rather than using the federal HealthCare.gov site, your closing deadline might be extended. For example, states like California, New York, New Jersey, and Washington, D.C. historically extend their final enrollment buffers out to January 31. Always verify your exact zip code parameters on the master portal early.

3. Medicare & Corporate Employer Windows

- Medicare Annual Enrollment: Runs on a completely different cycle, opening on October 15 and strictly locking down on December 7.

- Employer-Sponsored Plans (W-2 Jobs): These windows are set individually by corporate HR departments, but they almost universally occur across a brief 2-to-3 week window between October and November. If you miss your company’s internal portal window, you will automatically default to your previous selection or lose coverage entirely.

4 Strategic Tips to Outsmart the Insurance Algorithms

Insurance companies spend millions building algorithms designed to maximize their profitability per user profile. To win the comparison game, you need to look at your coverage options like a data analyst.

Tip 1: Hunt for Hidden Cost-Sharing Reductions (CSRs)

If you source your insurance through the ACA exchange and your household income sits anywhere between 100% and 250% of the Federal Poverty Level, bypass the cheap Bronze tier entirely and click directly on the Silver Plan tab.

Silver is the only metal tier legally eligible for Cost-Sharing Reductions. These are automatic government-funded upgrades that alter the internal mechanics of the plan. When you select a Silver plan within this specific income bracket, the system will artificially slash your individual deductible from thousands of dollars down to a few hundred bucks, while lowering your maximum out-of-pocket exposure. You essentially secure a premium Gold-tier policy for a deeply discounted Silver price tag.

Tip 2: Build an HSA Tax Shield

If you are generally healthy, don’t take expensive daily specialty medications, and only see a doctor for routine checkups, your best financial configuration is a High-Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA).

By selecting an HSA-compatible policy, you can legally funnel pre-tax money into a dedicated health investment account. For individuals, you can shield up to $4,400 (or $8,750 for families) from Uncle Sam. That cash goes in tax-free, grows completely tax-free via investment options, and comes out tax-free to pay for medical expenses. It is the only financial account in America that features a triple-tax advantage.

Tip 3: Audit the “Formulary” Line Items

Never pick a plan based solely on a low monthly premium if you take regular prescriptions. Every single insurance carrier maintains a proprietary document called a formulary—a master list that categorizes medications into distinct pricing tiers (Tier 1 being cheap generics, Tier 4 being expensive brand-name specialties).

Before checking out, open the plan details, type your exact prescription dosage into the provider portal, and confirm which tier it falls under. A plan that costs $20 less a month in premium is a massive net loss if it shuffles your daily medication into a non-covered or high-coinsurance category.

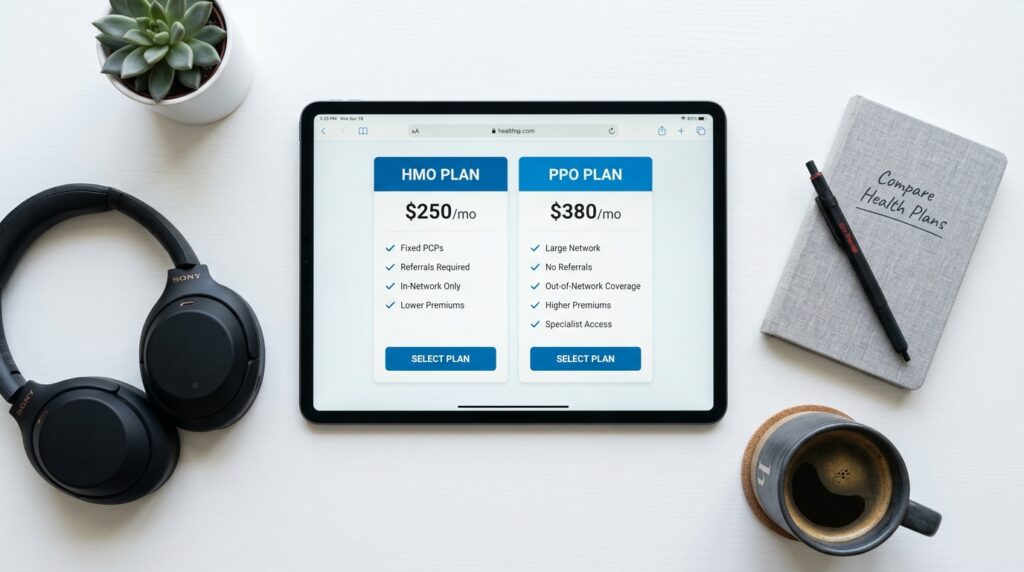

Tip 4: Map Your Regional Network Architecture (HMO vs. PPO)

Understand the gatekeeper rules of the plan you are purchasing before you sign the contract:

[ Network Types ]

│

┌────────────────┴────────────────┐

▼ ▼

[ HMO ] [ PPO ]

───────────────── ─────────────────

• Cheaper premiums • Higher premiums

• Strict local network • Nationwide freedom

• Primary Doctor required • No referrals needed

• $0 Out-of-Network cover • Partial Out-of-Network cover

If you travel extensively or have a trusted specialist you cannot afford to lose, paying the premium premium for a PPO (Preferred Provider Organization) is non-negotiable. If you select a cheaper HMO (Health Maintenance Organization) and see an out-of-network provider, your policy will pay exactly zero percent of that medical bill.

The Best-Performing Insurance Plans Across Major Segments

While health insurance performance is highly localized by state and county borders, three national carriers consistently secure top marks based on recent national J.D. Power customer satisfaction indices and NCQA quality ratings.

1. Blue Cross Blue Shield (BCBS) / Anthem: Best for Massive Network Freedom

If you value nationwide accessibility and want to ensure almost any hospital you encounter accepts your insurance card, BCBS remains the golden baseline standard. Their PPO network footprint is the largest in the country, making them the premier choice for families, frequent travelers, and independent remote workers.

2. Kaiser Permanente: Best for All-In-One Integrated Care

Kaiser operates on a unique structural model: they are both the insurance company and the physical hospital system. If you live in their coverage footprint (predominantly across the West Coast, Colorado, and parts of the Mid-Atlantic), Kaiser consistently dominates clinical quality rankings. Everything from your primary doctor, lab work, radiology, and pharmacy lives under one single roof, making the consumer administrative experience incredibly seamless.

3. Oscar Health: Best for Digital-First Convenience

Built explicitly for a tech-forward demographic, Oscar excels if you want to manage your entire healthcare ecosystem from a clean mobile app interface. They offer free, 24/7 virtual urgent care access directly through their smartphone dashboard and feature dedicated digital “Care Teams” that help you locate local providers and clear up billing disputes via a direct text interface.

Step-by-Step: How to Execute Your Open Enrollment Audit

Don’t wait until December 14 to scramble through your paperwork. Follow this exact sequence to ensure your finances are optimized before the closing gate locks:

1.Download Your Current Claims History:Takes 10 mins.

Log into your current insurance member portal and pull your “Explanation of Benefits” (EOB) log for the past 12 months. Total up exactly how much you actually spent out of pocket on copays, prescriptions, and specialist visits. This real data forms your baseline for next year’s needs.

2.Calculate Your Projected MAGI:The most critical metric.

Gather your tax documents and project your Modified Adjusted Gross Income (MAGI) for the upcoming year. If you are self-employed, remember to subtract your legitimate business deductions from your gross revenue to find your net profit—entering an inflated gross figure will cause you to lose out on thousands of dollars in premium subsidies.

3.Access the Official Exchange Portal:Bypass predatory spam sites.

Navigate directly to HealthCare.gov (or your official state exchange portal). Plug in your zip code and your newly calculated MAGI. The system will automatically display your personalized government subsidy, lowering the listed monthly premiums in real-time.

4.Verify Network Alignment and Bind:Finalize and confirm.

Run your primary doctor’s name through the specific directory of the new plan you like. Once confirmed, finalize the selection, opt for automatic paperless billing, and confirm that you receive a digital policy confirmation number before the closing deadline.

3 Critical Mistakes to Avoid This Cycle

- Relying Blindly on “Passive Enrollment”: Letting your current plan auto-renew without checking the market is an incredibly expensive mistake. Even if your health needs haven’t changed, insurance carriers frequently drop doctors from their networks, alter their drug formularies, or adjust their underlying deductibles from one year to the next. Spend the 30 minutes to review the new policy specs manually.

- Falling for Unregulated “Health Share” Entities: If you see an option online that claims to offer comprehensive health protection for an unbelievably low, flat rate of $80 a month, look at the fine print. These are frequently “Healthcare Sharing Ministries” or fixed indemnity plans. They do not comply with the Affordable Care Act, are legally permitted to deny coverage for pre-existing conditions, cap your lifetime payouts, or refuse to cover mental health services entirely. Stick exclusively to compliant plans hosted on the official government exchanges.

- Miscalculating the “Subsidy Cliff”: If you are close to the upper eligibility tiers for financial marketplace credits, monitor your business or salary income meticulously. Crossing an income bracket by even a single dollar can trigger an sudden termination of your advanced tax credits, meaning the IRS can claw back those monthly discounts directly out of your tax refund when you file your annual paperwork.

Final Thoughts

Open Enrollment can feel like an incredibly tedious administrative chore, but it is one of the most impactful financial windows of your entire year. Health insurance should never be treated like a fixed utility bill that you just blindly pay. It is a highly flexible, customizable financial shield.

Set a firm notification on your calendar for early December, pull up your current claims data, log onto the official exchanges, and actively control the math. Your physical health and your bank account will thank you down the road.