When I registered my first official LLC, I felt completely invincible. I had the state approval documents in a crisp folder, a fresh Employer Identification Number (EIN), and a business bank account with a modest balance. I genuinely thought that the “Limited Liability” part of my LLC was an invisible, magical shield that protected me from every corporate disaster imaginable.

Then, I landed a contract with a client who wouldn’t even let me look at their staging server until I uploaded a Certificate of Insurance (COI) proving I had a $1,000,000 General Liability policy.

That was my wake-up call. I realized the hard way that while an LLC protects your personal assets (like your house or your personal savings) from business debts, it does not protect your business assets from lawsuits, client errors, or property damage. If your LLC gets sued and you don’t have insurance, your business bank account can be completely wiped out, effectively killing your dream.

So, I spent days hunting down quotes, filling out endless online forms, and talking to brokers. Over the years, as my business grew, I tested different platforms and insurance carriers. If you are looking to protect your LLC right now, you don’t have to guess which provider is legitimate. Let’s break down the top five business insurance providers for LLCs based on real-world usability, speed, and pricing.

The Top 5 LLC Insurance Providers Compared

Finding the right provider depends heavily on what your LLC actually does. A single freelance software developer needs completely different coverage than a local residential roofing LLC or a boutique retail store. Here is how the top five players stack up in the current market.

| Provider | Best For | Standout Feature | Online Quote Speed |

| NEXT Insurance | Best Overall for Digital & Solo LLCs | 100% digital management & instant digital COIs | Under 10 minutes |

| The Hartford | Best for Established & Scaling LLCs | Over 200 years of experience; best for professional services | 10–15 minutes (or via agent) |

| Thimble | Best for Gig Workers & Micro-LLCs | Ultra-flexible coverage by the month, day, or hour | Under 5 minutes |

| biBERK | Best for Direct-to-Consumer Savings | Backed by Berkshire Hathaway; bypasses the middleman broker | Under 10 minutes |

| Hiscox | Best for Tailored Professional Liability | High-end customization for specialized consultants | 10–15 minutes |

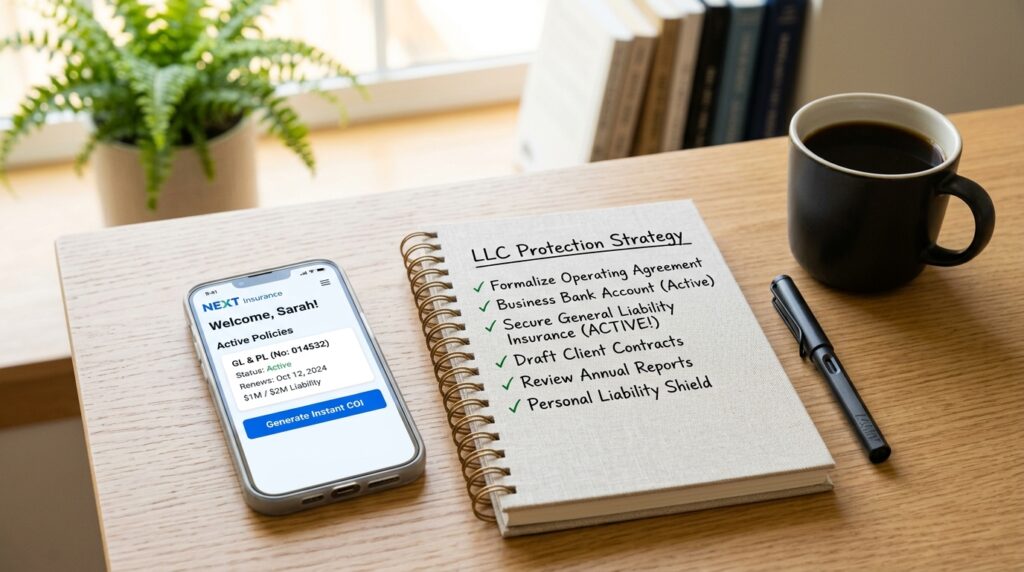

1. NEXT Insurance: Best Overall for Digital & Solo LLCs

If you are a modern creator, e-commerce seller, freelancer, or run a small agency, NEXT Insurance is usually the easiest starting point. They were built from the ground up for the internet age, meaning they cut out the old-school corporate friction.

- The Experience: Running a search on NEXT is entirely painless. You don’t have to wait for an agent to call you back on a Tuesday morning. You input your LLC details, answer a few basic risk questions, and get a price.

- Why it fits LLCs: Their dashboard lets you generate unlimited, customized Certificates of Insurance (COIs) for free, instantly. If a new corporate client demands their name be added to your policy as an “Additional Insured” before an event or project, you can log into the mobile app and send it over in less than two minutes.

- The Cost Baseline: For a standard single-member consulting or tech LLC, NEXT often clocks in as the price leader, sometimes hovering around $40 to $50 a month for a baseline policy.

2. The Hartford: Best for Established & Growing LLCs

If your LLC has physical office space, expensive inventory, or a handful of W2 employees, you might want to look at an industry titan like The Hartford. They have been around since 1810 and protect over a million small businesses.

- The Experience: While they do offer online quoting, their true strength lies in their comprehensive bundling. If you need a complex Business Owner’s Policy (BOP) that ties together General Liability, Commercial Property, and Workers’ Compensation, their underwriting handles it beautifully.

- Why it fits LLCs: The Hartford dominates when your headcount crosses 5 or more employees. Their pricing matrices scale incredibly well for larger team structures, whereas digital-first platforms can sometimes get expensive when you start adding massive payroll numbers to Workers’ Comp policies.

- The Cost Baseline: Expect to pay closer to $100 to $150+ a month here, but that usually reflects a sturdier, multi-policy bundle designed to withstand significant real-world exposure.

3. Thimble: Best for Gig Workers and Seasonal LLCs

Thimble completely flipped the insurance industry on its head by introducing short-term, on-demand business insurance.

- The Experience: Imagine you run a photography LLC, a landscaping business, or an event planning service. You don’t work year-round, or maybe you only take on three or four large corporate gigs a year. Paying a massive annual premium feels like burning money. Thimble allows you to buy insurance strictly for the days, weeks, or months you are actually working.

- Why it fits LLCs: It keeps your overhead incredibly low when you are in the proof-of-concept phase of your business. If a city park requires insurance for a weekend pop-up market your LLC is hosting, you can buy a policy just for those 48 hours.

- The Cost Baseline: If you buy a standard monthly policy, it is very comparable to NEXT (around $50 to $90 a month), but their micro-policies can cost as little as a couple of bucks an hour depending on the job risk.

4. biBERK: Best for Direct-to-Consumer Pricing

If you like the idea of a massive, rock-solid financial institution backing your business but hate paying middleman broker fees, biBERK is your answer. They are part of the Berkshire Hathaway insurance group (yes, Warren Buffett’s empire).

- The Experience: Because biBERK insures businesses directly without traditional brokers taking a commission cut, they pass those savings straight down to the business owner. The online portal is clean, simple, and completely unbloated.

- Why it fits LLCs: Many large corporate clients or government entities require your insurance carrier to have an “A++” financial strength rating before they will sign a contract with you. Because biBERK has the massive financial weight of Berkshire Hathaway behind it, your COI will pass any corporate legal team’s vetting process instantly.

- The Cost Baseline: They are fiercely competitive, often undercutting traditional independent brokers by 15% to 20% for direct General Liability and Workers’ Comp policies.

5. Hiscox: Best for Specialized Professional Liability

If your LLC provides high-consequence advice, specialized consulting, engineering blueprints, or sensitive data management, you face a lot of “intellectual” risk. If a client claims your strategy directly cost them fifty grand, General Liability won’t save you—you need Professional Liability (Errors & Omissions). Hiscox is the undisputed king of this niche.

- The Experience: Hiscox excels at tailoring policies to hyper-specific industries. When you go through their questionnaire, they ask intelligent questions specific to your exact trade rather than throwing you into a generic “professional services” bucket.

- Why it fits LLCs: They understand micro-businesses and solo operators deeply. They won’t force you to buy massive commercial packages you don’t need just to get the core professional liability protection your contracts require.

- The Cost Baseline: Professional liability is inherently riskier than general slip-and-fall insurance, so policies here typically run between $50 and $100 a month depending on your exact specialty.

Step-by-Step: How to Choose and Bind Your LLC Policy

Don’t let the paradox of choice paralyze you. Buying a policy shouldn’t take more than an afternoon if you follow this basic workflow:

1.Define Your Minimum Contract Requirements:Step 1.

Check your client contracts or your commercial lease agreements. Do they require a $1M policy or a $2M policy? Do they require you to have property insurance (a BOP)? Know your numbers first.

2.Run Fast Quotes on NEXT and biBERK:Step 2.

Spend 15 minutes plugging your LLC info into NEXT and biBERK. This instantly establishes your absolute baseline market price for a modern, direct policy.

3.Evaluate Your Physical Risks:Step 3.

Do you have inventory? Do you have tools? If yes, look at bundling a BOP through The Hartford or biBERK to ensure your physical assets are covered alongside your liability.

4.Set a Smart Deductible:Step 4.

If money is tight, opt for a $1,000 deductible. It keeps your monthly premiums manageable without putting your business in a massive cash-flow hole if you ever actually have to file a claim.

The Million-Dollar Mistake to Avoid

The single biggest mistake I see new LLC owners make is underreporting their projected annual gross revenue to save twenty bucks a month on their premiums.

Insurance companies aren’t stupid. Many policies are subject to a premium audit at the end of the policy year. If you tell an insurer like NEXT or The Hartford that your LLC is only going to make $20,000 this year, but your business ends up crushing it and pulling in $200,000, they will audit your financial records at the end of the year and hit you with a massive, unexpected bill for the premium difference. Be honest about your projections from day one.

Final Thoughts

An LLC is a fantastic tool for separating your personal life from your business life, but it isn’t an insurance policy.

If you are a solo operator running a clean, digital business, jump on NEXT Insurance or biBERK and get a policy bound today so you can pitch clients with confidence. If you are scaling a team or moving into a physical commercial space, let The Hartford build you a proper, bulletproof bundle. Spending $50 a month to protect everything you are building isn’t just a cost of doing business—it’s the cheapest peace of mind money can buy.